Accounting And Its History

This is the first article of our series of intensive series of articles to make understand Accounting and its concepts in a simple and efficient way. Lets get started with the term Accounting and its history.

History & Meaning of Accounting

Accounting is a general act done by everyone in the day to day life.

Accounting is very important because it is the language of the business and its transactions, its results how it is communicated to the people.

Accounting is the systematic and comprehensive recording of financial transactions related to a business.

Accountancy is the process of measuring, processing and communicating the financial information or economic information about the business entities and corporations.

Accounting provides the necessary information and facilitates better decisions by investors, management etc. In general terms Accounting is the answer for “How much has been spent and how much has been earned and by what means?”

The main intention or the expectation of the investors is:

- What is the investment being spent for?

- How effectively is my investment being spent?

- How much is the company earning with my money and how much is it paying back?

All the above questions of the investors can only be answered by business through a process called “Accounting”.

Accounting is defined as “the art of recording, classifying, and summarizing in a significant manner and in terms of money, transactions and events which are, in part at least, of a financial character, and interpreting the result thereof” by the committee setup by the AICPA (American Institute of Certified Public Accountants).

Accounting is the Language of business as it measures, classifies and communicates the result of the amount spent by a business. It is also referred to as the ideology of the management or the managers and the way of earning return.

Accounting in business view is defined as comprehensive recording of financial transactions related to a business. Accounting process starts from the point when the money is spent and summarizing the transactions, understanding and analysing the transactions, categorizing them and reporting them to the respective authorities or persons. It defines a business and its functioning. It explains the reason or the force the business is driven or sustaining i.e whether the business is sustaining due to the efficiency of the management or the employees or the investors or creditors or the processes. Accounting, through its results motivates the management and the businesses to work and run effectively. People who do the process of accounting for a business are called as “Accountants”.

Stages of accounting history

There are four stages of accounting history. The first stage began in primitive period and the most recent stage is still continuing in present time. These stages are mentioned below:

Emergent

This stage began in the primitive days and lasted till 1494. The very first book describing double-entry accounting and debit and credit entries was published in 1494 as well.

Preanalytic

The second stage of accounting, Preanalytic period started in 1495 and ended in 1799. During this stage some of the key accounting concepts were introduced. These concepts include going concern, money measurement and periodic inventory.

Development

This stage lasted from 1800 to 1950. The primary shifts to take place during this stage were a manufacturing-based economy and multiple business shareholders.

Modern

Starting from 1951 to the present civilization, it is the modern accounting era. In this era, we have been introduced to some of the important issues, such as stock market crash of 1929 and ethics investigations.

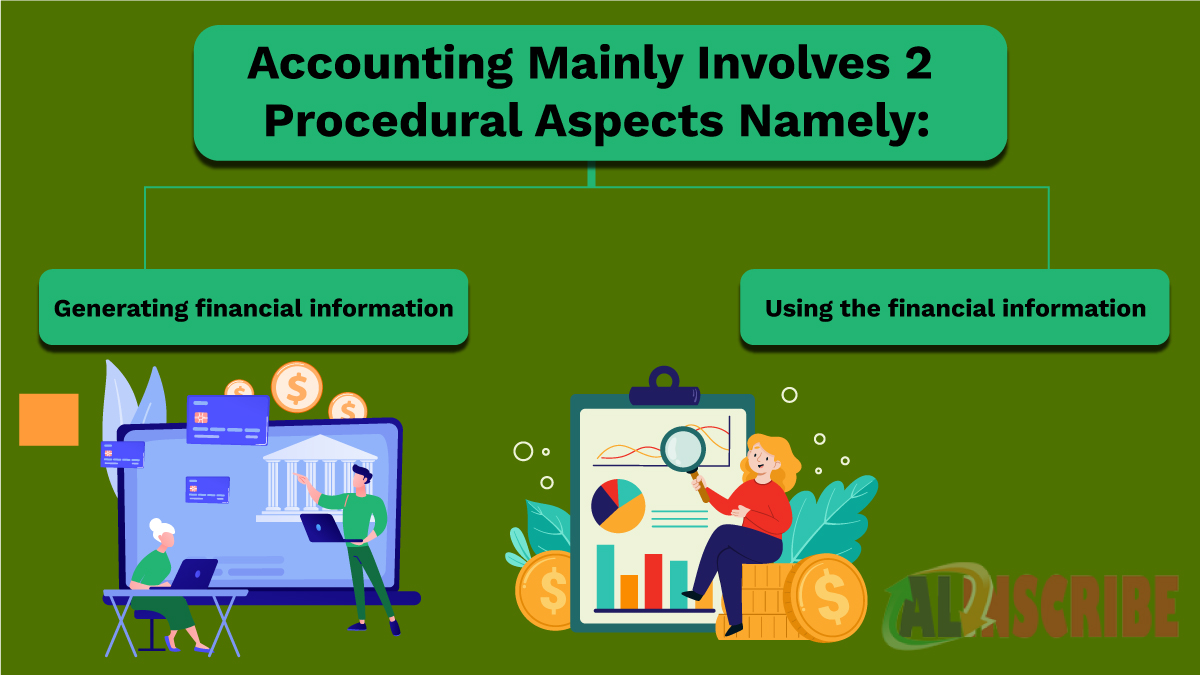

Accounting mainly involves 2 procedural aspects namely:

- Generating financial information and

- Using the financial information.

1. Generating financial information is the duty of accountants by the process of accounting i.e through identifying the transactions, summarizing them, measuring and classifying them, analysing and interpreting it into a meaningful manner so as to be used by managers or users of financial statements or the stakeholders.

2. Using financial information is done by a large people or stakeholders, broadly called Users of financial information like the managers to assess the productivity of the processes, costing techniques, by the lenders or investors or shareholders to assess the return and the earning capacity of the investment in the company, by the creditors for assessing the credit worthiness of the company and the authorities for tax assessment.

Accounting can be sub divided into many sub fields like Financial accounting, Management accounting, Tax accounting, and Cost accounting. Accounting is largely facilitated by accounting organizations, accounting firms and professional bodies. Accounting involves usage of many principles, conventions, policies in the preparation and presentation of financial statements. The items in the financial statements are mainly guided by the Accounting standards, Generally Accepted Accounting Principles (GAAP). These GAAP are set by benchmarked institutions like Financial Accounting Standards Board (FASB) in the United States and in UK, the Financial Reporting Council. Accounting basically sets a benchmark for the financial information to be compared and measured either inter-firm, intra-firm, inter-industry or intra-industry.

Article Comments

Similar Articles

Articles Search

Sponsor

Featured Articles

Most Popular Articles

Article Categories

There are zero sub-categories in this parent category.

There are zero sub-categories in this parent category.